The growth in renewable energies has coincided with a trend toward the digitalization of major infrastructure, often referred to as Industry 4.0. Artificial intelligence and machine learning (AI/ML), IoT devices such as sensors, the cloud and advanced communications networks are all combining to digitally transform the critical infrastructure we depend upon, making it smarter, more efficient, and more responsive. In the power-distribution space, these technologies are playing a crucial role in the smart grid, but they are also playing a role in power generation, including wind farms.

Wind farms 4.0

Unlike much established industrial infrastructure — which has, for the most part, missed the digital revolution — wind power has employed digital technologies from the start. And yet, innovation in this area is ongoing, and wind farms will be able to profit from these new technologies to achieve further efficiencies, improve asset management and maintenance, and improve worker communications for greater reliability and safety.

One of the key drivers for digital transformation has been the growth of broadband communications capacity. We have seen enormous capacity gains made using fiber optics and the replacement of many older communications systems by IP networks. Both these technologies are being widely adopted by wind farms. Fiber optics are often bundled with power cables to transmit supervisory control and data acquisition (SCADA) communications used to monitor and control turbines. SCADA and other industrial control protocols such as Modbus and Profinet are supported by IP/MPLS networks, which can also be used for a host of new IP-based applications.

Unlike much established industrial infrastructure, wind power has employed digital technologies from the start. (Courtesy: Nokia)

Converged communications

The consolidation of communications onto IP is also happening in broadband wireless networks based on 4G/LTE and 5G. This convergence means IP-based applications are now supported end-to-end by the communications network, whether wired or wireless. This converged broadband IP connectivity is the de facto platform today for Industry 4.0 applications.

Along with SCADA and industrial control protocols, even legacy applications such as basic voice communications — which today depend on TETRA or P25 private radio systems to link wind-farm workers — are being replaced by private LTE and 5G. The advantage of LTE and 5G is the ability to not only support push-to-talk, but push-to-video, as well as other kinds of high bandwidth communications, such as augmented reality (AR).

With their extra data capacity, these new systems allow field engineers to receive work orders and instructions digitally and be guided in the servicing of equipment by remote experts. They also can provide improved situational awareness to first responders in emergency situations by sending on-site video and even the biometric information of workers at the remote site through LTE-connected wearable devices.

Sensor analytics

Wirelessly connected sensors can monitor much more than the health and safety of individual workers. Sensor technologies can be deployed widely on any of the equipment used on the wind farm, from cranes to vessel, to the towers, turbines, and blades in order to improve asset management and maintenance.

Sensor data, which can include temperature, vibrations, audio/acoustics, humidity, and current, can be analyzed by machine learning software to create digital models of any kind of equipment and its normal behavior. This makes it possible to go beyond scheduled maintenance, to better understand the actual condition of assets, and whether they need to be maintained sooner or later. As data accumulates over time and the digital models of the equipment improve, it even becomes possible to predict failures in advance.

These kinds of software analytics systems can also be used for video footage, turning CCTV cameras into intelligent sensors. Scene analytics software can be used to spot any changes in the normal scene captured by a camera, identifying anomalies, such as an intruder approaching a turbine at a time when there is no work scheduled or counting animals such as deer or even hikers who might be walking in the area.

Alternative energy source. Floating wind turbines in sea and scheme

Anomalies that are spotted by the machine learning system can send a flag to remote personnel for review, with insights and footage that help to prioritize and address the issue. Scene analytics can also be used for audio data, so that microphones can, for instance, register changes in the pitch of the blade that might indicate a maintenance issue. Taking all these kinds of sensor data together and modeling their behavior over time, software analytics can predict when certain kinds of faults might occur based on the monitoring of environmental conditions and turbine performance. A topical use case, currently in trials, is being able to predict the build-up of ice on turbine blades, allowing operators the time to stop and heat the blades before failure occurs.

Pervasive wireless broadband can also be used to control drones for turbine inspection on offshore wind farms. The capacity of LTE, which is many times that of a very-small-aperture terminal (VSAT), allows high-definition video to be transmitted from the drone for close inspection of possible faults, such as stress fractures and other indicators of potential failure. It can also be used to control the drone remotely or beyond the line of sight where local regulations permit. These capabilities will only improve with the arrival of 5G.

Conclusion

Industry 4.0 technologies are being assessed by most industrial sectors for their potential to increase efficiency, productivity, and safety. It is an area of tremendous research and innovation led by cutting edge technologies such as machine learning and broadband wireless communications. We are only at the beginning of what will turn out to be the digital transformation and automation of the systems we rely on for everyday life. Wind power is also playing a rapidly growing role in the transformation of our energy infrastructure. The marriage of these two trends will help to ensure our energy will be cost-efficient, safe, and sustainable.

USA Rare Earth praised the introduction in the House of a bipartisan bill that would boost production of rare earth permanent magnets.

The new legislation would incentivize the domestic production of neodymium boron (NdFeB) rare earth permanent magnets that are used in electric vehicles, renewable energy, and the defense industrial base.

USA Rare Earth owns 80 percent of the Round Top Heavy Rare Earth, Lithium, and Critical Minerals Project in Hudspeth County, Texas. (Courtesy: USA Rare Earth)

“USA Rare Earth applauds the introduction of the Rare Earth Magnet Manufacturing Production Tax Credit Act and efforts by Congress to restore this critical U.S. production capability. These incentives would be a boost to U.S. manufacturers and would help establish a beachhead for NdFeB magnet production in the U.S. The legislation also reflects the urgent demand by automakers for the rare earth magnets necessary to transition to zero-emission vehicles by 2030, and it underscores the importance of the parallel requirements for the U.S. defense industrial base,” said Pini Althaus, CEO of USA Rare Earth.

USA Rare Earth, LLC owns 80 percent of the Round Top Heavy Rare Earth, Lithium, and Critical Minerals Project in Hudspeth County in west Texas. Round Top hosts critical heavy rare earth metals including lithium, zirconium, hafnium, and beryllium.

U.S. Reps. Eric Swalwell (D-CA) and Guy Reschenthaler (R-PA) authored the bill. They are co-chairs of the Congressional Critical Materials Caucus.

“This bill would spur domestic manufacturing and reward innovation, and it would help re-shore a vital U.S. supply chain with potential for international collaboration. Led by the chairs of the Congressional Critical Materials Caucus, the bill dovetails with the whole-of-government approach under way to swiftly secure U.S. supply chains and to restore NdFeB magnet manufacturing in the United States,” Althaus said.

Once operational, USA Rare Earth’s NdFeB magnet plant will produce at least 2,000 tons each year of rare earth magnets, accounting for about 17% of the (2019) U.S. permanent magnet demand.

The U.S. lacks a commercial-scale capability to process rare earth permanent magnets used in the automotive, aerospace, defense and electronics industries. At present, no other NdFeB permanent magnet manufacturing plant is operational in the United States.

Siemens Gamesa will expand its offshore blade factory in Hull, England by 41,600 square meters, more than doubling the size of the manufacturing facilities. The expansion represents an investment of £186 million and is planned to be completed in 2023.

Siemens Gamesa is expanding its offshore blade factory in Hull, England. (Courtesy: Siemens Gamesa)

“Since our offshore blade factory opened in Hull in 2016, Siemens Gamesa has proudly served as the catalyst for the powerful growth the area has seen. The rapid development of the offshore wind industry – and continued, strong, long-term support provided by the UK government for offshore wind – has enabled us to power ahead with confidence when making these plans. We’re committed to unlocking the potential of wind energy around the globe, with solutions from Hull playing a vital role,” said Marc Becker, CEO of the Siemens Gamesa Offshore Business Unit.

The blade factory is the largest offshore wind manufacturing facility in the UK.

Manufacturing of next-generation offshore wind turbine blades will grow to 77,600 square meters and add 200 additional direct jobs to the approximately 1,000 person-workforce already in place.

“The UK government has provided strong and consistent support for offshore wind, having committed to a further 30 GW installed this decade, three times the current installed capacity,” said Clark MacFarlane, Managing Director of Siemens Gamesa UK.

Deutsche WindGuard Inspection has completed recurring inspections on 30 wind turbines at the offshore wind farm Global Tech I in the German North Sea, which is owned by Global Tech I Offshore Wind GmbH.

Global Tech I is about 180km northwest of Bremerhaven, Germany. The inspection included towers and nacelles, in accordance with the Standard Design of the Federal Maritime and Hydrographic Agency (BSH).

Deutsche WindGuard Inspection has completed recurring inspections on 30 wind turbines at the offshore wind farm Global Tech I in the German North Sea. (Courtesy: Deutsche WindGuard Inspection)

“We are pleased that Global Tech I Offshore Wind GmbH counts on our expertise and has commissioned us with the inspection of the technical condition and safety equipment,” said Jan Wallasch, managing director of Deutsche WindGuard Inspection.

“With the highest level of thoroughness, our experienced offshore experts carefully inspected this year’s inspection scope of 30 turbines and also checked the monitoring and maintenance documentation. For this purpose, the team was stationed on board of the REM Inspector service vessel directly in the wind farm for four weeks in June,” Wallasch added.

“The working environment in the offshore wind farm is very dynamic because of sudden weather changes, among other things,” said Frederik Modes, Head of Operations & Maintenance Wind Turbines Global Tech I Offshore Wind GmbH.

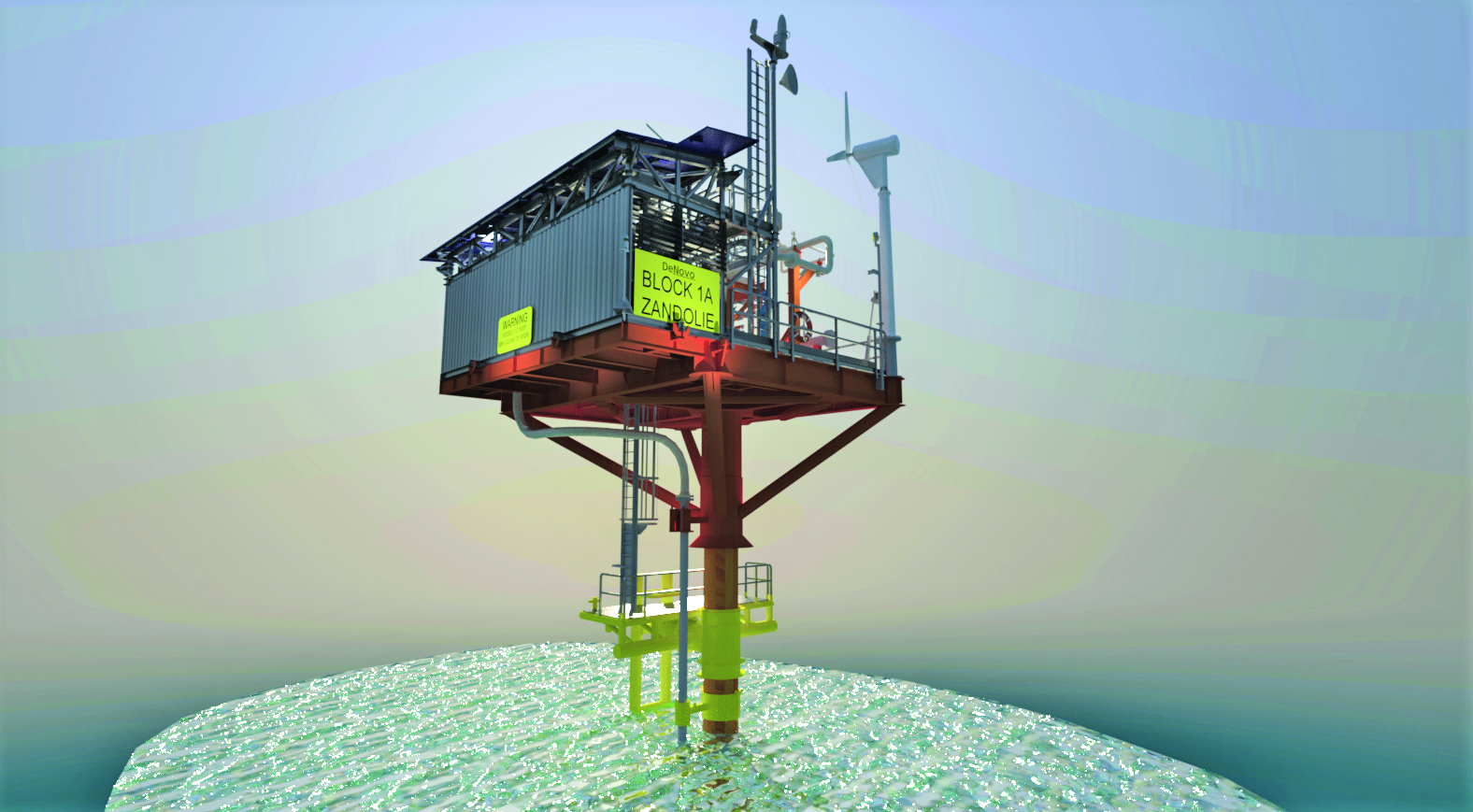

Aquaterra Energy has completed the engineering design for DeNovo Energy Limited’s Sea Swift offshore platform, a part of development activity in the Gulf of Paria off the west coast of Trinidad.

The platform, which will be self-powered by a wind turbine and a solar bank, is set to be installed in Q4 of this year, in water depths of 20m.

Aquaterra Energy has completed the design for DeNovo Energy’s Sea Swift offshore platform. (Courtesy: Aquaterra Energy)

“Intelligent engineering is at the heart of what we do, so this renewable-powered solution is a testament to our ethos,” said Stewart Maxwell, Aquaterra Energy technical director.

The platform design will include a battery to store excess power, which eliminates the need for traditional diesel generators—which reduces emissions, including those resulting from refueling visits.

Monitoring technology will reduce maintenance trips by requiring personnel to visit only when alerted by onshore systems.

Another cost reduction in the Sea Swift design is drilling and installation via a jack-up rig, which removes the need for a heavy lift vessel.

The platform’s reduced steel requirement and its focus on using infrastructure that is in local Trinidad and Tobago area adds to the increase in speed toward the platform’s first oil or gas production.

“DeNovo is committed to securing Trinidad and Tobago’s energy future—in a cleaner way,” said Bryan Ramsumair, DeNovo managing director.

Leosphere has launched WindCube Complex Terrain Ready, to deliver wind measurement in terrains from moderate to the most complex.

The offering includes Leosphere’s patented Flow Complexity Recognition (FCR) software, and the Computational Fluid Dynamics correction method to deliver accurate and trusted measurement.

WindCube Complex Terrain Ready delivers wind measurement in terrains from moderate to complex. (Courtesy: Vaisala)

“With wind energy being one of the fastest-growing sources of sustainable energy production, the location of wind farm development and operations have expanded to new and challenging environments,” said David Pepy, Leosphere’s head of renewable energy.

“This expansion into hilly, mountainous and other areas with varying levels of terrain complexity, make it challenging to collect trusted and precise wind measurements that illustrate what the wind is doing in these increasingly complicated locations. That’s where our solutions come in to ensure project operators realize precise data in all types of complex terrain,” Pepy said.

With WindCube Complex Terrain Ready, companies have easy access to both FCR and CFD correction services, empowering wind farm developers with accurate, reliable, bankable, and widely accepted wind flow data. The integrated FCR solution is appropriate for moderately complex terrain while CFD post-processing, available as an option through partnerships with wind energy leaders and consultants, is leveraged for more complex terrain. In some cases, customers use both FCR and CFD data to ensure the highest possible wind measurement outcomes.

The company has partnered with proven CFD industry leaders, including Meteodyn and WindSim, and wind energy consultants such as ArcVera, Deutsche WindGuard, DNV, Fraunhofer IWES, and UL, to ensure WindCube customers have access to the right CFD solution and industry expert support to meet their specific needs.

Gazelle Wind Power Limited has raised $4 million toward the development of its hybrid floating offshore wind platform. The investment includes $1.3 million in seed funding and $2.7 million in long-term financing that will be used to develop Gazelle’s first grid-connected demonstrator.

Investors include Spanish businessman Valentin de Torres-Solanot del Pino, as well as Peter Murphy and Zach Mecelis, co-founders of Covalis Capital.

Gazelle Wind Power Limited’s hybrid floating platform surmounts the current barriers of buoyancy and geographic limitations while reducing costs and preserving fragile marine environments. (Courtesy: Gazelle Wind Power Limited)

“Gazelle has the potential to completely change the offshore wind industry. By combining the best features of tension-leg and semi-submersible platforms — while eliminating their drawbacks — Gazelle’s technology will be at the forefront of tomorrow’s energy landscape. The E2IN2 team is delighted to join Gazelle and contribute in its efforts to carry out this invaluable undertaking,” said de Torres-Solanot del Pino.

The Dublin-based company’s hybrid mooring platform is designed and engineered by naval engineers to enable floating offshore wind production in deeper waters farther out at sea. The patented design allows for a 70 percent reduction in the weight of steel, while delivering a stable platform with a tilt of less than one inch, together with a 30 percent cost reduction compared to other floating wind platforms.

Gazelle recently named a group of energy industry veterans to its board of directors, including leading global policymakers, government officials, engineers, and CEOs. The board includes Javier Canada (current CEO of Highview Power); Jon Salazar, a former senior advisor with Deloitte; Pierpaolo Mazza, formerly of GE Power Generation; Connie Hedegaard, Denmark’s former environment minister; and David Mesonero, who was CFO at Siemens Gamesa Renewable Energy.

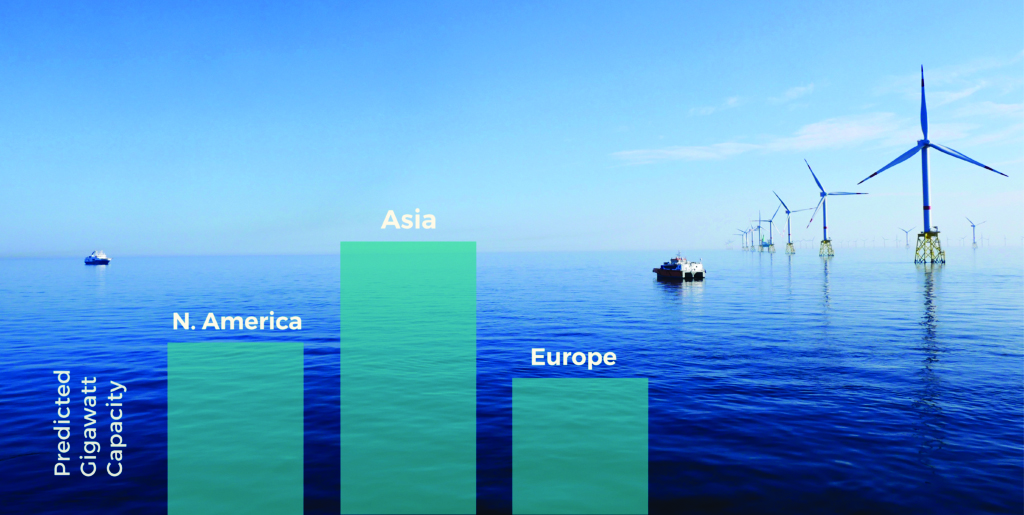

Demand for wind farms will increase over the next decade, according to offshore wind analyst Zac Ward.

In 2020, spending on offshore renewable projects was higher than that of offshore oil and gas spending, by an estimate of $12 billion, with $43 billion for oil and gas and $56 billion for renewable energy.

Asia is predicted to be the leader in gigawatt capacity in the next 10 years. (Courtesy: VesselsValue)

Newly built vehicles and repurposed or upgraded supply vessels will meet the demand for wind farm installation and maintenance vessels.

While the global capacity for offshore wind farms is now at 25GW, that number will rise to 235GW by 2030, estimates say.

VesselsValue’s Orderbook shows that out of the renewable energy still on order, about half is for Europe and half are for the Far East.

The United Kingdom has the most wind farms installed, followed by Germany, China, Denmark, Belgium, and the Netherlands. Asia, however, has the highest number of future plans for wind farms.

VARD, a major global designer and shipbuilder of specialized vessels, has announced contracts with Norwegian shipping company Rem Offshore for two Construction Service Operations Vessels (CSOVs) with an option for two additional vessels. The contracts for the two vessels total 100 million euros.

The CSOVs are ideal for service and maintenance operations at offshore wind farms. VARD’s 4 19 design is a versatile platform for offshore wind farm support, with a focus on onboard logistics, security, and comfort.

Rem Offshore and VARD have signed contracts for the design and construction of two Construction Service Operations Vessels (CSOVs), with an option for two more. (Courtesy: Rem Offshore)

VARD is set to deliver the first vessel in the first half of 2023. It will be delivered from VARD in Norway, while Vard Tung in Vietnam will deliver the second vessel in 2024.

“We are proud to be chosen as the preferred partner for Rem Offshore in this exciting project, and we are looking forward to working together with their team. These contracts confirm VARD’s leadership in the CSOV market, both in terms of innovative ship design, breakthrough technologies and shipbuilding quality,” said VARD CEO Alberto Maestrini.

With a length of 85 meters and a beam of 19.5 meters, the vessels will have a height-adjustable motion-compensated gangway with elevator system, a height-adjustable boat landing system, and a 3D-compensated crane. The CSOVs will accommodate 120 on board.

VARD’s specialized high-tech subsidiaries will be involved with major deliveries onboard, and in the vessels’ shipbuilding process.

“Rem Offshore has during the last few years increasingly focused attention on building a sustainable platform for growth in offshore wind. Our shareholders are driving this development together with our Rem colleagues onshore and offshore.

We are proud to continue our newbuild program in Norway and support the local maritime industry,” said Aage Remøy, chairman of Rem Offshore.

The American Clean Power Association recently announced it would be merging with the U.S. Energy Storage Association. What was the thinking behind this decision so soon after the recent merging of other renewables under one roof as ACP?

ACP was created with the mission to unite the voice of all clean-energy technologies — wind, solar, and energy storage.The merger with ESA is a natural progression in fulfilling ACP’s mission to present a unified voice across various technologies.

After months of thoughtful discussion and collaboration, the Boards of ACP and ESA both agreed to the terms for a plan of merger for our organizations to combine our resources and reach starting in 2022.

The value both boards see our organizations providing to one another is two-fold; adding storage expertise to ACP’s work and bringing numerous new resources to bear for storage advocacy for ESA members.

How will the merger enhance the American Clean Power Association’s efforts to advocate for the economic and environmental advantages of the clean-power economy?

As ACP continues to position itself for multi-technology advocacy, acquiring ESA’s existing team and membership is an attractive alternative to building a new storage team and competing for limited membership resources.

The deep expertise and structure of ESA coupled with the reach and resources of ACP will ensure stronger advocacy on behalf of the energy-storage industry and the broader clean-power sector.

Wind turbine in the water park for offshore energy

What steps are you taking to promote the positive nature of the merger?

ESA has been holding several informational sessions with its members, and ACP has actively participated in those sessions to answer questions and expand upon the services and structure of ACP.

Both the ESA and ACP boards unanimously endorsed a merger, and we have collectively spent the last several weeks providing information and further details with ESA’s members.

What does the merger mean for the industry and its goal to achieve 100 GW of new energy storage by 2030?

We see a lot of growth over the next decade. In a world increasingly focused on addressing the climate crisis, the prospects of the renewables and storage industries will be increasingly intertwined.

As a part of ACP, storage industry interests will have the backing of greater resources and a seat at the table for higher-profile policy engagements that no single technology could attain on its own.

A unified voice among our industries sends a stronger message to policymakers and the public about the critical role storage will play for years to come.

ACP will advocate strongly for the energy storage industry’s No. 1 priority — a standalone investment tax credit (ITC) for energy storage.

ACP also has the resources to have an increased focus on the other priorities necessary to reach 100 GW of storage by 2030 including international trade and market design topics.

What about this new partnership will aid in giving a more unified voice to the renewables sector?

The clean energy sector has historically been very segmented — with a proliferation of groups competing for limited resources.

The merger of ACP and ESA creates a more unified voice on behalf of energy-storage interests and unites the industry resources to push for meaningful gains both across the clean energy sector and for energy storage specifically.

Once the merger goes into effect January 1, 2022, what will that mean for trade shows and other events?

Both ACP and ESA will continue to have their annual events and tradeshows as planned in 2021, and we look forward to supporting each other’s events as named supporters.

With the final approval by ESA’s membership, we will work collaboratively to determine the best suite of events for 2022 and beyond — including any energy-storage specific events that are beneficial to the sector.

We are looking forward to reconnecting, reenergizing, and returning to our trade shows and other events in the future.

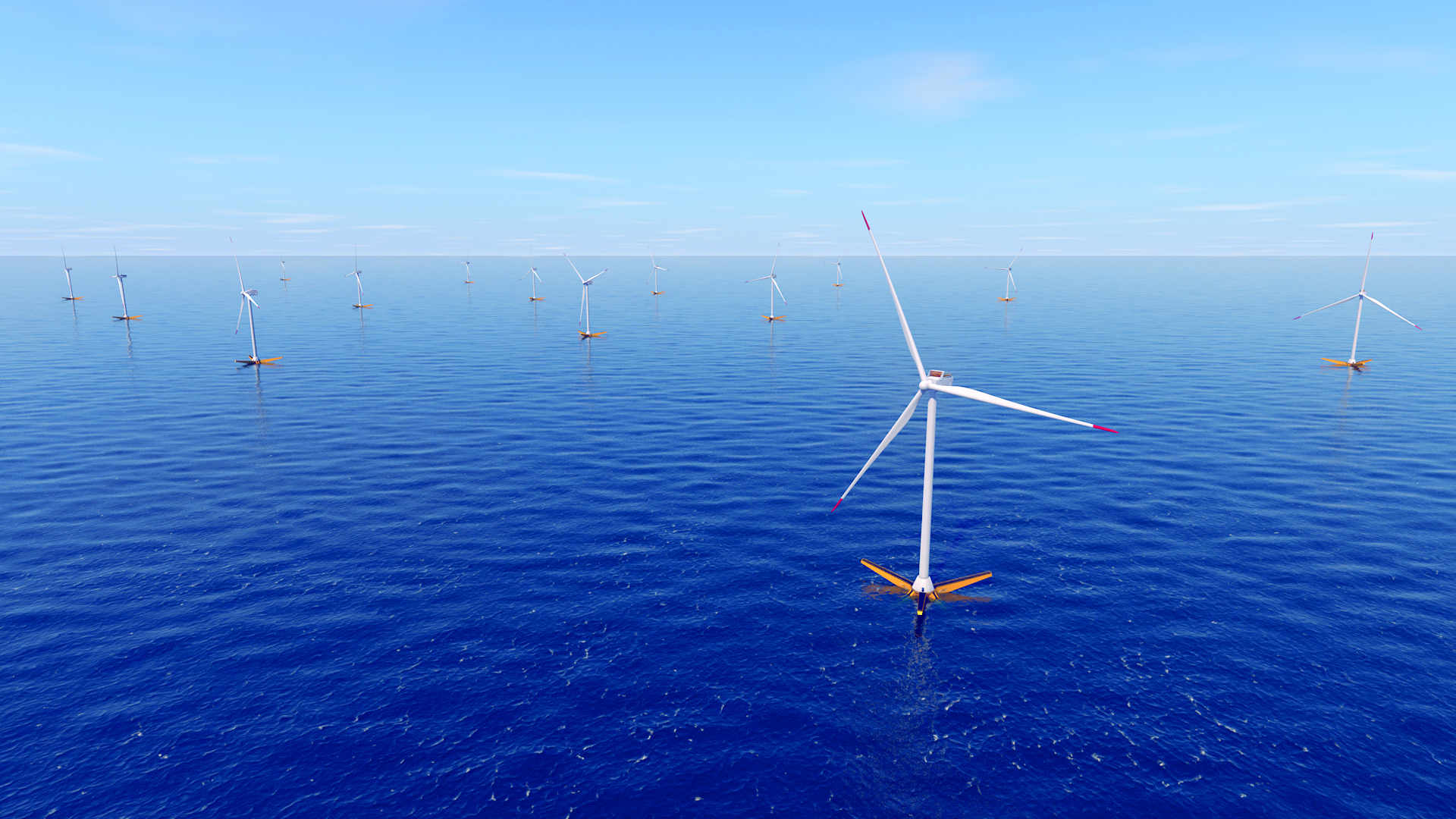

Offshore wind is taking a firm hold in Europe, and in the U.S., it’s dawning as the next big thing in wind energy. But for all the talk about offshore wind, it’s mostly fixed wind turbines that are getting most of the attention.

The minds behind Cerulean Winds, however, said that fixed turbines only scratch the surface of offshore wind’s potential, and floating offshore wind turbines are the true wave of the future, offering massive potential.

“Floating wind is the last mover advantage in the wind industry, because the opportunity for floating wind is far, far bigger and has far more potential, and actually, in some respects, it’s far better because it’s further offshore,” said Dan Jackson, co-founder of Cerulean Winds. “The winds are stronger, and you’re not interfering with many of the near-shore issues associated with fishing and leisure use and birds and the environment. Our projects are hundreds of miles offshore, and that presents a far better solution in every regard.”

Cerulean’s integrated 200-turbine floating wind and hydrogen development could halve UKCS asset emissions from 2025. (Courtesy: Cerulean Winds)

Oil and gas background

In working with getting turbines spinning offshore, Cerulean Winds brings a background of oil and gas expertise, as well as integrated contracting, according to Jackson.

“The vast majority of offshore wind projects, not floating, but offshore fixed wind — which is what it’s been today — still have a fairly piecemeal approach to contracting where the owners take the majority of the risk,” he said. “Our construct is bringing in Tier One contractors as part of the integral part of the proposition. They’re investors in the scheme. And they work as an integrated contract. The integrated contracting is very much part of the proposition in financing from the infrastructure markets. These are part of the proposition. And deep-water oil-and-gas expertise in floating structures and mooring systems is crucial for the success of floating wind.”

Cerulean Wind’s expertise with oil and gas is what led to its current involvement with floating wind as it reaches a technical maturity, according to Jackson.

“The endeavors of others in the various pilot programs have been very successful,” he said. “The motions of floating foundations have very little impact on the turbines and the performance of the turbines. And they also, more importantly, demonstrate that, even in harsh offshore environments such as the north of Scotland, where some of the pilot programs have been, the motions of these space frame structures are very consistent with the understanding from oil and gas and actually pretty benign.”

Cerulean’s proposal is for three sites, two in the Central North Sea and the other West of Shetland, among the most hostile environments in the world.

“The right sort of floating structure with the right mooring systems is 100 percent reliable in that environment,” Jackson said. “There are oil-and-gas installations in the same location that back that up.”

Driving force of floating wind

The need for floating wind becomes clearer with a quick look at coastlines around the globe where they drift off pretty quickly into deep water, according to Jackson.

“Deep water in the wind space is probably 50 meters, but most places don’t have long shallow water shafts,” he said. “In the U.S., I think we see a number of things. What we’re doing in the U.K., we’re concentrating on one particular effort, which is decarbonization of the oil and gas facilities. We are looking at the same in the U.S., as an opportunity, and we certainly see the same enthusiasm by the oil and gas companies to decarbonize their industrial facilities, both onshore and offshore. It’s not just the big platforms offshore, but it’s also where the oil and gas comes to shore — some pretty dirty industrial real estate.”

Cerulean Winds’ proposition is to power offshore facilities with electricity from floating wind. (Courtesy: Cerulean Winds)

That can all be cleaned up with green-power generation at a large commercial scale, according to Jackson.

“We are looking at the U.S., and we see the entry points being the decarbonization of existing industrial facilities that are important for everybody — particularly the climate lobby — to decarbonize the real mess that’s out there as well as obviously provide green energy to the grid and to power people’s homes and onshore industrial plants,” he said. “There are some easy wins, and the easy wins are to decarbonize bad polluters in industrial end users.”

Major project in the works

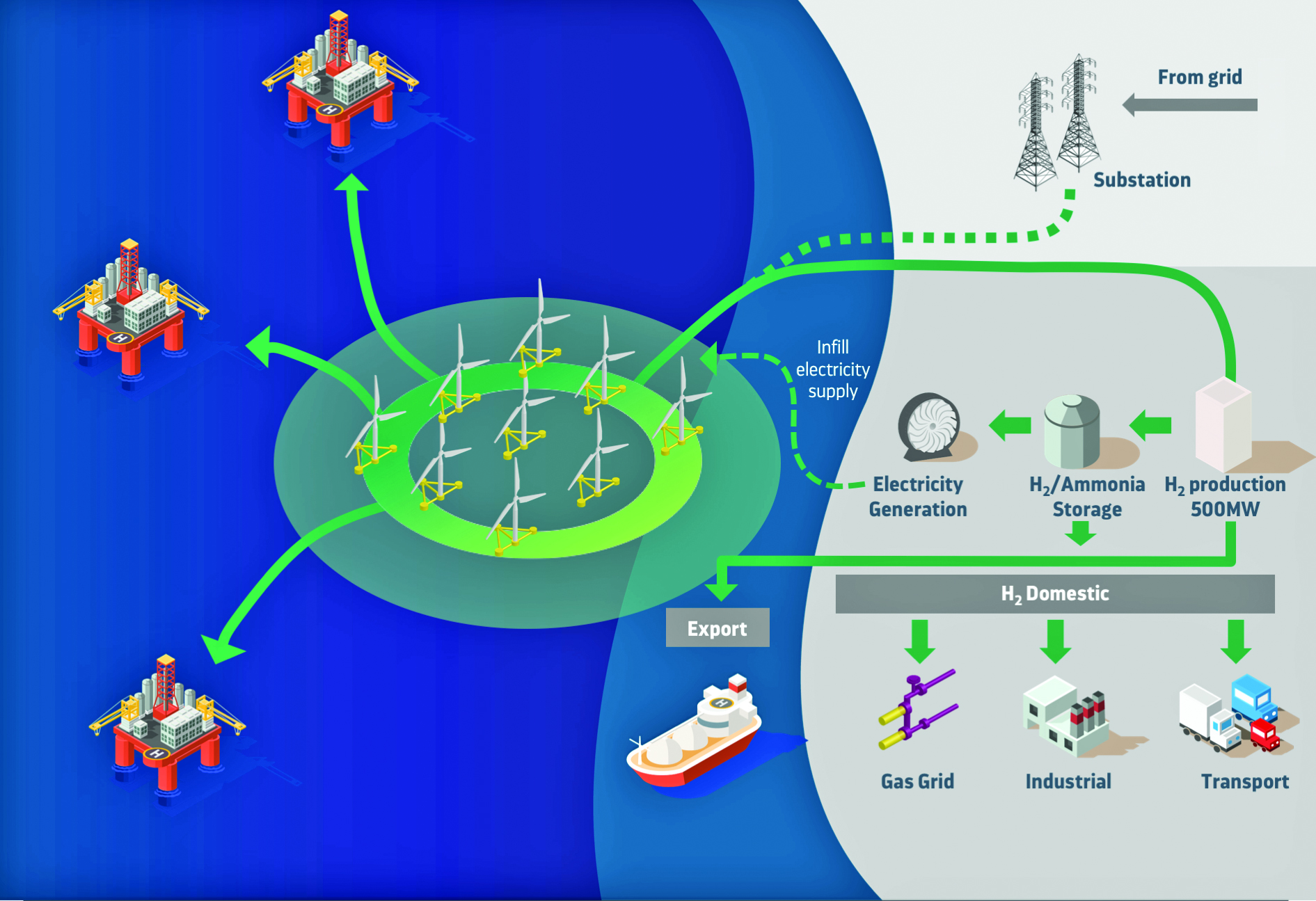

Turning offshore wind on a commercial scale into reality is Cerulean Wind’s main objective, and, to best illustrate that point, Jackson said a Cerulean project includes three 1-GW wind farms connected together to provide green energy to large industrial facilities. Those facilities include offshore oil and gas platforms and onshore industrial users that would use the extra green energy produced to provide green hydrogen.

“We have, in the U.K. scheme, proposed three green hydrogen plants, each of which are 500-MW nameplate capacity,” he said. “Within Europe, those plants are not the largest by far; there are quite a number of green hydrogen plants in process under contract in that bracket. The floating wind farms we’re proposing are three 1-GW plants. The fields are the largest in the market, and they need to be of that scale to have an impact on the upstream oil and gas facilities to cut the emissions. That would cut 10 million tons of carbon dioxide emissions a year from the oil and gas facilities on the U.K. continental shelf and produce large amounts of green hydrogen in the U.K.”

The green hydrogen economy is an important focus of the U.K.’s directive, according to Jackson. There are a lot of similarities between what the European countries are doing. The U.K. is probably marginally ahead of others, but what the U.K. is proposing is being looked at by Germany and Denmark as well as by Japan and the U.S.

“There’s a real political shift now that floating wind, in particular, is commercially viable,” said Jackson. “It’s very comparable to large-scale fixed wind offshore in terms of price per megawatts. And that opens up all sorts of opportunities to go from floating wind to green hydrogen as a private system.”

The turbines are custom-built for extreme environmental conditions. (Courtesy: Cerulean Winds)

Continually pushing net-zero future

By pushing these directives not just in the U.K., but worldwide, Cerulean Winds’ goal is to move power generation globally from fossil fuels to renewable energies, according to Jackson.

“And it can happen at scale in a very short period of time,” he said. “By the end of the decade, we should see the majority of the power being generated in the developed world using renewable energies. It can happen that quickly. It’s a shift. It’s a shift that needs to happen. And I think public sentiment has now been understood by the political leaders, and political sentiments are driving through the regulation, opening up the processes for developers, such as Cerulean, to bring in large-scale infrastructure schemes.”

“We are creating an offshore transmission system,” he said. “And that offshore transmission system consists of both offshore power generation and, secondly, the movement of power through an offshore transmission network. There are many analogies, for example, in the U.S. Gulf where there is a fantastic gas transmission system and a fantastic oil transmission system. And the next stage is actually complementing these with a power transmission system where ultimately the renewable power generation will replace fossil fuel extraction.”

Infrastructure player

Cerulean Winds tackles these challenges as an infrastructure player, according to Jackson.

“We aligned ourselves with certain partners, and so, there are two sets of partners that are very important,” he said. “We have a set of Tier One contractors that can deliver the infrastructure. We’ve declared, for example, NOV, which is a U.S. contractor for the floating units, in our view the best marine contractor in the floating wind market. And we’ve locked in the other Tier One contractors to deliver the schemes that we’re proposing. The U.K. scheme I’m referring to is in excess of 10 billion pounds. It’s a proper mid-scale infrastructure play.”

The second piece is the financing, according to Jackson.

“It was very important before we went to the regulators or started proposing schemes, that we could demonstrate that we had confidence to deliver the funding from the infrastructure markets for the proposition,” he said. “It’s an infrastructure play, where the infrastructure will be installed, and the end users, the oil and gas facilities, the industrial users, or the hydrogen plants will just be charged the tariff for the electricity. The same as what you pay at home — just pay for what you use. And the infrastructure is paid for by the financial markets.”

A hydrogen industrial economy

There has been a lot of talk about heavy industries in Europe such as the steel industry, moving to a hydrogen economy, according to Jackson. Those industries need gas to get the temperatures from all their processes, but they are looking for ways to do it in a green way. Green hydrogen is a solution to keep those industries going, but it does it in a way that is acceptable to the current world view.

“There’s an overwhelming demand for green energy,” he said. “But there’s also a serious bottleneck with the grid system in most countries in the world. The grid system was designed in the ’50s and not for the 2020s looking forward. So, the reinforcement of the grid is a separate project for every country. But what we’re doing is taking green energy produced by large-scale floating wind and using it either for direct application to industrial to decarbonize industrial facilities like oil and gas platforms, or we’re using it to generate green hydrogen, which is a very transportable and usable product. We see these integrated energy schemes as economically robust, and they’re the solutions that work. What doesn’t work is just another wind farm, putting more green energy into a grid that’s already bottlenecked.”

The wind farms are sized to ensure 100 percent availability to oil and gas assets most of the time. (Courtesy: Cerulean Winds)

‘Poster child’

And although Cerulean Winds has concentrated its efforts mostly in the U.K., mainly because it has progressed the furthest in the market, it offers entry points for others, according to Jackson.

“The regulators are using Cerulean as a poster child, if you like, for what’s possible,” he said. “They’re certainly using our schemes as ways of bringing the regulators together. In the U.S. and other fast developing markets, it’s the same as there are many different stakeholders in the regulatory framework. And floating wind is something that crosses many different regulators. There is no floating wind regulator in the U.K., nor is there any dedicated floating wind regulator anywhere in the world. It crosses a number of maritime regulators and maritime rules and specifications and regulations. And it crosses, obviously, the renewable sector as well as marine planning, and many other departments within the civil service and the government.”

And what the U.K is doing, in common with other governments, is trying to get those different regulators to work together for the development of floating wind, according to Jackson.

“It’s no different in places like California,” he said. “It’s not the same as saying this is just another wind farm. It’s a floating structure. There are a whole bunch of things that are very different. And one of the things we’re very proud of is the fact that the Cerulean proposition is being used as a test case over here to help pull regulators together.”

That will help maneuver Cerulean Winds into a market-leader position in the floating wind space, according to Jackson.

“I think floating wind is a massive opportunity for wind,” he said. “Offshore wind is fast maturing. It became economically viable and now it’s economically robust, and everybody with a coastline wants offshore wind for all those reasons. Floating wind is the best part of offshore wind because it’s further offshore, more stable, capitalizes on bigger winds and has more flexibility on water depth. Floating wind is going to be a big part of the offshore wind industry, and the offshore wind industry has really only just started.”

With a global pandemic wreaking havoc and uncertainty on so many industries over the last 18 months, anyone watching the news would expect it to also have a negative impact on the renewables sector. But, surprisingly, that has not been the case — at least, not in Canada.

Robert Hornung, president of the Canadian Renewable Energy Association, said that, even though renewable growth was low in 2020, it was not a product of pandemic-related issues.

“It really was a product of: That’s not when we were expecting those projects to be built,” he said. “We knew going into 2020, it would be a lower year. And we knew that in 2021, we would start to see it pick up, and that’s what’s happened.”

Projects deployed in 2020 included about 170 MW of wind installed and a little more than 60 MW of solar installed; however, that below-normal growth was due more to the timing of contracts in Canada at the time, according to Hornung.

“That build-out is generally occurring as a result of contracts that have been awarded through RFPs,” he said. “And it just turned out that a lot of these COD dates were not in 2020.”

More than 500 MW of wind and solar have been installed in the first half of 2021. (Courtesy: CanREA)

13,500 MW of wind in 2020

Those small numbers still pushed Canada to end 2020 with more than 13,500 MW of installed wind capacity, which left Canada in the top 10 worldwide, according to Hornung. And the country’s solar capacity ended 2020 with more than 3,000 MW, pushing Canada into the top 20.

But six months into 2021, Canada is getting back to a more normal renewable growth schedule.

“We’ve already had more than 500 MW of wind and solar installed in the first half of 2021, and we expect to be close to a gigawatt by the end of the year,” Hornung said. “We expect similar things in 2022. And frankly, I only expect to see that accelerate going forward as Canada has now legislated a net-zero by 2050 climate-change commitment. There are discussions about establishing a target date for decarbonizing the grid in Canada. And, with the cost competitiveness of these technologies as new demand appears, we’re quite confident that there are a lot more opportunities emerging.”

So, although COVID did have an impact on the industry in terms of supply chain issues, Hornung stressed the pandemic did little to slow industry growth or make people think twice about renewables in general.

“We saw the industry respond very well, I think, in terms of taking action to protect the health and safety of their own employees going forward through COVID,” he said. “I think we have a lot of examples of wind and solar projects working within the communities that they’re based in to provide COVID-related financial assistance and support, as well as our companies being good citizens in these communities as we worked through this.”

Growing renewables in Alberta

A large part of why renewables continue to have a strong presence in Canada is the development of corporate PPAs in Alberta, and how they are driving the market.

In order to see exactly what that means to the Canadian market, Hornung said it’s necessary to review what drivers stimulate the development of renewable energy.

The first driver is the increased demand for electricity, which was hit by COVID. In many parts of Canada, the need for growth was hindered by an electricity surplus, particularly in provinces with large hydroelectric resources.

The second driver is a need to decarbonize the grid, but with Canada’s grid already 80 percent decarbonized, the pressure to develop renewable energy sources isn’t as strong as it is in the U.S., where there’s still a drive to move coal out of the energy equation.

Although there is a growing corporate demand for renewables in other parts of Canada, it is more of a challenge due to vertically integrated utilities. (Courtesy: CanREA)

The third driver is corporate.

“In Canada, the only jurisdiction where we have a deregulated market that enables, in an easy way, these bilateral power purchase agreements to be signed between customers and renewable energy providers is in Alberta,” Hornung said. “And so, in Alberta, we have seen commitments made this year for over 800 MW of new wind and solar through corporate PPAs. When you think about that, in 2021 overall, we’re going to install close to a gigawatt, this is a pretty significant number. And it’s growing steadily, and is a reflection of Alberta having really good quality wind and solar resources and a unique market structure in the Canadian context, which enables these bilateral agreements. We’ve had some big names coming in to do this, including Amazon and Budweiser.”

Vertically integrated utilities

Although there is a growing corporate demand for renewables in other parts of Canada, it is more of a challenge due to vertically integrated utilities, according to Hornung.

“In most other parts of the country, we have vertically integrated monopoly utilities, and so there’s only one potential customer to buy renewable power,” he said. “But we’re starting to see some innovation there as well. Nova Scotia, one of our smaller provinces, has started a green choice program where they have canvassed the corporate community in Nova Scotia, identified the demand for wind and solar and have, as a result, said, ‘We’re going to move forward with a procurement in our system to bring those resources online so that those customers can actually secure that power.’ It’s a green tariff kind of scenario. And we expect to see more of that across the country going forward as corporate demand grows.”

Because of Canada’s market structure, corporate PPAs are not the same driver in Canada as they may be in the U.S. or even in Europe, but they have become a tremendous driver in Alberta and are encouraging other jurisdictions to think about what they can do to respond to that demand, according to Hornung.

Another reason that makes these procurement opportunities so lucrative for Alberta in particular is that the province has Canada’s most carbon-intensive electricity grid.

“That’s why you’re seeing a lot of activity there, but two other provinces where coal is still playing a significant role are Saskatchewan and Nova Scotia,” Hornung said.

“Saskatchewan just awarded a 200-MW contract for new wind this year and has said that they will be looking for more wind in the future. And Nova Scotia just announced an RFP for 350 MW of renewables going forward as they’re working to phase out coal-fired generation by 2030.”

Projects deployed in 2020 included about 170 MW of wind installed and a little more than 60 MW of solar installed; however, that below-normal growth was due more to the timing of contracts in Canada at the time. (Courtesy: CanREA)

Enter Quebec

And although Canada has a legislative requirement to phase out coal by 2030, a new driver involving electrification is coming into focus, and Hornung said Quebec is working to turn that driver into a reality.

“Quebec is a province that has the most aggressive electrification strategy in the country in terms of promoting electric vehicles, promoting increased use of electricity in buildings, and promoting increased electricity use in heavy industry, for example, in aluminum smelters,” he said. “And because of that electrification strategy, they have now determined they’re going to see electricity demand grow after many years of having surpluses, and, therefore, they need to procure more electricity. Quebec has come forward, and they have announced that they will be releasing a 300-MW RFP for wind this fall, and they’ve already signaled that they’ll need another 1,400 MW going forward.”

That means, with all the surplus energy in Canada, the real growth opportunity for decarbonization will come with increased demand arising from electrification and green hydrogen as the country continues to get more serious with its climate commitments, according to Hornung.

“We’re starting now to see some of those initiatives bear fruit in terms of raising expectations for increased demand for electricity going forward,” he said. “And we’re confident, because of the cost competitiveness of wind and solar, that no matter where you are in Canada, because of these well-distributed resources, when demand goes up and you’re going to need to build new generation, there’s a pretty solid chance that you’re going to be looking at wind and solar just on cost alone.”

A large part of why renewables continue to have a strong presence in Canada is the development of corporate PPAs in Alberta. (Courtesy: CanREA)

Addressing the grid

This will also mean expanding the grid, according to Hornung.

“When we look at dealing with climate going forward, it means we’re going to have to decarbonize the grid, and in all likelihood, we’re going to have to double the size of the grid in order to meet those needs,” he said. “And you’ve got an increasing amount of evidence coming forward that people expect that the new electricity need is going to be dominated by wind and solar because of their cost-competitiveness.”

To help make his case, Hornung pointed to the International Energy Agency’s net-zero report released this year. In the report, the IEA said that between now and 2050, it expected wind and solar to move from 9 percent of global electricity to 68 percent.

“That means that a lot of the new build is wind and solar,” he said.

Earlier this year, a joint study of the U.S., Canadian, and Mexican governments looked at how to get aggressive greenhouse gas emission reductions within the grid, according to Hornung. The study looked at scenarios where Canada largely decarbonizes its grid by 2050, and it concluded that 90 percent to 95 percent of new electricity builds in Canada would be wind and solar.But a tremendous amount of investment will be required to fundamentally transform and expand the grid, according to Hornung.

“The pressures to do that in the most cost-effective way are going to be enormous,” he said. “And that is really going to strengthen the hand of wind and solar. I mean, the IEA report this year called solar the new king of electricity, the lowest cost source of electricity ever.”

But with that “call to arms,” so to speak, a tremendous amount of optimism is growing within the sector, according to Hornung.

“There are significant opportunities coming,” he said. “The barriers, I think, to capitalizing on those opportunities, won’t be technology barriers, they’re barriers related to regulatory systems and market rules. Can we have our markets and regulatory frameworks catch up to the innovation that has enabled disruptive technologies like wind and solar to allow them to be deployed at the size and the scale that’s going to be required if you’re serious about meeting targets like net-zero greenhouse gas emissions by 2050?”

In that vein, evolving technology is actually making great strides in keeping costs down, according to Hornung.

Lazard, a financial advisory and asset management firm, has said in the last decade, solar costs have declined 90 percent; wind costs have dropped 70 percent, and battery storage costs have been reduced by 90 percent.

“Everyone expects those costs to continue to go down — not at that rate, but they will continue to go down going forward, and that will be a product of ongoing technological evolution,” Hornung said.

The COVID-19 pandemic did little to slow industry growth. (Courtesy: CanREA)

Investing in the electricity systems

Beyond the technology advancements being developed, costs will also need to be looked at from a system perspective as well, according to Hornung.

“When we bring all of this wind and solar onto the grid, that’s going to require significant investment within the electricity system to ensure reliability and manage variability,” he said. “This is where we’re going to see a lot of disruptive technologies that will really open up new opportunities to find ways to keep costs down. So, when we talk, for example, about integrating wind and solar going forward, well, one thing you want to do is build transmission. There’s obviously a lot of discussion in the U.S. about transmission. But it’s also important to think about how to make our existing transmission more efficient. That’s where technology like energy storage can play a tremendous role. If your transmission line is only at full capacity less than 10 percent of the time, can storage actually allow you to work through that so you don’t have to build new transmission?”

New disruptive technologies include distributed energy resources such as solar on the rooftops of homes and businesses, the introduction of electric vehicles to people’s driveways, and a wide range of demand response technologies, according to Hornung.

“All of these things are going to offer system operators more choices, more options for managing the grid,” he said. “It’s our view that when you have more options and more choices and if you allow competition between them, you’re going to get lower costs as a result. If we modify and evolve our regulatory frameworks and market frameworks to ensure that those technologies are considered and have an opportunity to provide services to the grid, I’m quite sure the net benefit is going to help to keep costs down as we go through this energy transition.”

Making opportunities

And as Canada moves into 2022 and beyond, it will become even more necessary to ensure there are comprehensive strategies in place that encourage electrification and facilitate the use of green hydrogen, according to Hornung.

“Because, if the demand is there, there will be opportunities that the industry can respond to,” he said. “If the demand is not there, then it doesn’t matter if you’re cost competitive or anything else, nobody’s going to want to buy the power. But I think the industry is extremely well positioned to respond to that demand as it emerges. Are we going to implement the actions required to create this new demand for our technologies? Are we going to say in Canada, like the Biden administration has said, we’re going to work to decarbonize the grid by 2035? Are we going to ensure in Canada that our carbon pricing systems send a really clear market signal that says, ‘You should be favoring less emission-intensive technologies’?”

‘Implementation time’

The good news is Canada has strong milestones in place in terms of what the country needs to achieve and when, according to Hornung.

“We know, from a tremendous amount of research and analysis, what we need to do to get there — and now, it’s implementation time,” he said. “Are we going to move as a country from just talking about taking action on climate change and setting targets without following through on implementing them to actually taking action? If we are serious about taking action, I have absolutely no doubt that wind and solar will be front and center in that effort.”

And the arrival of the Biden administration only serves to open up more opportunities for collaboration between the U.S. and Canada, according to Hornung.

“There’s a lot of evidence that this is already occurring,” he said. “We’re already seeing agreements to collaborate with respect to minerals required for renewables and electric vehicles. The recent North American Renewable Integration Study very clearly demonstrates that, with both Canada and the U.S. trying to reach aggressive greenhouse gas emission reduction targets and decarbonize their electricity grids, increased electricity trade between the two countries is critical to help reduce costs. And both countries have clearly expressed an interest in exploring that and taking advantage of those opportunities.”

Editor’s note

Electricity Transformation Canada is CanREA’s annual conference and is expected to attract key stakeholders looking to advance the global electricity transformation to Toronto from November 17-19, 2021. Participants will include utilities, system operators, governments, end-use sectors undergoing electrification, and a variety of energy professionals. For more information, go to electricitytransformation.ca.

The offshore wind industry has yet to reach its full potential. But, over the last 10 years, innovative designs and advanced technology has lowered the levelized cost of energy (LCOE). Even with this rapid progress, offshore wind is still in its infancy as a go-to energy production and consumption source.

Recent advancements have allowed wind developers to literally venture into deeper waters. Farther offshore, we can harness the full potential of wind and use it to bring clean energy to transmission grids in regions worldwide.

Some already have begun to see the monetary, environmental, and ecological benefits floating wind farms in waters deeper than 60 meters can provide — especially when compared to bottom-fixed offshore wind structures. To realize its full potential, wind developers need to address several performance-related issues so offshore wind components in deeper waters obtain cost-effective designs that achieve favorable performance while maintaining structural integrity.

From top to bottom, how can floating offshore developers make the most of their wind farms?

According to the International Renewable Energy Agency (IRENA), the average size of offshore wind turbines grew by a factor of 3.4 in less than two decades. Courtesy: Gazelle Wind Power. All Gazelle images are artistic impressions and purely for illustrative and confidential purposes.

Performance of Turbines and Towers

According to the International Renewable Energy Agency (IRENA), the average size of offshore wind turbines grew by a factor of 3.4 in less than two decades and is expected to grow to an output capacity of 15 to 20 MW by 2030.

Modern wind turbines are becoming more cost-effective and reliable over time, even with this steady increase in size and output. Increased cost-effectiveness and reliability are due to the more efficient use of steel, iron, and other materials like fiberglass used to produce them. The widespread adoption of 3D printing and modeling also reduces the time and labor-intensive process of constructing blades and turbine components. With fewer input materials and less manual labor required, implementing 3D printing and automation can easily allow developers to create component molds and turbine components quickly.

Software innovations also allow computer modeling, simulations, and data analysis to become a prevalent part of development, design, and construction. Software can be used to construct visual models and perform simulations to test performance in several different conditions while applying numerous external and internal factors. These tools allow for more thorough system analyses of every part of the turbine to better harness wind.

New technologies also allow developers to actively measure, model, and analyze how wind turbines interact with the grid. Retooling their concepts allows developers another opportunity to rethink the design and implementation of turbines before scaling up and increasing the number of units in a given wind farm.

While many wind developers are already using some or all of these tools and technologies in their design and manufacture of turbines, the standardization of these techniques will be critical to implementing more innovative, efficient, optimized designs.

The most prominent factors in increasing offshore wind performance are the structures and systems supporting the turbines and towers. Courtesy: Gazelle Wind Power. All Gazelle images are artistic impressions and purely for illustrative and confidential purposes.

Performance of Platforms and Mooring Systems

The most prominent factors in increasing offshore wind performance are the structures and systems supporting the turbines and towers. This is especially true for floating wind developers.

At depths greater than 60 meters, it becomes harder to build, secure, and maintain fixed platforms to the seafloor. Fixed structures also need more steel and concrete as they increase in size. The immediate solution to support larger towers and turbines are larger platforms, requiring more steel and/or concrete. Because of this, fixed platforms are harder to secure and less cost-effective in deeper waters.

Floating platforms remain the most viable solution to take full advantage of more robust, less intermittent winds farther from shore. However, the approach for reducing the load on the tower and turbine and decreasing the pitching motion associated with increased wave activity in rougher conditions is still a subject of debate.

The three most common floating platform concepts in the offshore wind industry are spar-buoy, tension-leg platform, and semi-submersible. Although there are additional concepts in the design and development phase, most designs are variations of these three concepts.

Developers should consider the pros and cons of these platforms before trying to implement a completely new design. It is essential to ask these questions:

What do these designs do well?

What factors affect their performance the most?

How do their mooring systems factor into their efficiency?

How are they constructed?

How are they transported?

How easy are they to maintain and repair?

Semi-submersible designs can be constructed onshore or in shipping yards and docks and transported to sites using conventional tugs. Still, they tend to use more steel and concrete than other floating designs and often have higher critical wave-induced motions.

Tension-leg platforms do not have the same problems with wave-induced motions.

Floating platforms remain the most viable solution to take full advantage of more robust, less intermittent winds farther from shore. Courtesy: Gazelle Wind Power. All Gazelle images are artistic impressions and purely for illustrative and confidential purposes.

Nevertheless, because they are highly buoyant, they can be difficult to keep stable during transport and installation — and also have a higher installed mooring cost.

Spar-buoy designs have a simple design and lower mooring cost, but they require heavy-lift vessels to put them in place and often cannot withstand rough conditions in waters between 60 and 100 meters.

The key to using the best of all of these concepts, without their drawbacks, goes back to an old adage: “Sometimes, less is more.”

Putting costs aside, larger structures that require more steel and concrete are not the answer. They are worse for the environment and require pontoons and specialized mooring systems to keep them buoyant. And even still, added buoyancy does not ensure optimal performance.

A hybrid floating platform that combines the best features of tension-leg and semi-submersible platforms eliminates some of the drawbacks of other floating wind platform concepts while allowing wind farms to be placed in deeper waters (potentially 400 meters or more). They also allow the platforms themselves to move vertically and horizontally with the wind and the waves. Rethinking the platform and mooring system designs could dramatically decrease the tonnage of steel and concrete needed by as much as 70 percent, allowing for lighter, more reliable structures.

Hybrid platform designs that use fewer input materials allow the platform to move with almost zero-pitch angle. Null pitch means reduced wearing, less maintenance, and ultimately leads to longer life of the turbine.

At greater depths, floaters need their own individual mooring systems. The greater the length or number of mooring lines each system has, the greater the chance that those lines fail. This could prove catastrophic for every unit in a given wind farm. Designs that use fewer mooring lines would allow for increased performance. Hybrid designs could use up to 80 percent fewer mooring lines (maximum loads) than standard tension-leg structures and 75 percent fewer mooring lines (length) than conventional semi-submersible designs.

Revamped mooring systems will also reduce loads — which ultimately reduces the size and costs of foundations and installation. It is possible to reduce horizontal movements of floating platforms by as much as 70 percent. Smaller horizontal movements mean smaller swept areas and less drift than many current designs.

Modern wind turbines are becoming more cost-effective and reliable over time, even with this steady increase in size and output. Courtesy: Gazelle Wind Power. All Gazelle images are artistic impressions and purely for illustrative and confidential purposes.

These lighter, smaller, efficient designs will allow for easier installation and commissioning — meaning standard-sized harbors, tugs, and cranes can all be used to construct all of the components and transport them to the site of the wind farm — with the potential to produce savings as much as 1 million euros per megawatt.

Implementing designs that address improvements to the turbines, platforms, and mooring systems will lead to increased effectiveness and longevity, which allows for less maintenance — meaning less risk and greater safety for the workers maintaining and repairing them. Additionally, turbine, platform, and mooring components in smaller, lighter structures can be brought into the harbor or shipyard for repairs and replacements, creating greater efficiency.

Final Thoughts

Increased efficiency will come with time as new technology will allow for a deeper scientific analysis on the performance of mooring systems, platforms, turbines, and other components — but developers should constantly be studying and rethinking their designs so the implementation of cleaner energy for a growing worldwide population can continue to accelerate.

The offshore wind industry is gaining momentum thanks to ambitious environmental targets, competitive costs, and huge market potential. This renewable source of energy provides an optimal load factor, minimizing the need for electricity storage or complementary dispatchable sources of energy. The public sector has been rushing the field with new players, including oil and gas companies, creating a strong push for investments in the wake of the COVID-19 crisis.

Ambitious national targets

Since the 2015 United Nations Climate Change Conference, most governments have launched energy transition strategies and are adopting a variety of approaches to decarbonize. [1] Historically, offshore wind development mostly took place in Europe in the North Sea, and China has set ambitious targets for offshore wind. But so far, the United States has been less ambitious. The European Union (EU) is aiming to install between 230 and 450 GW of capacity by 2050, and China announced 175 GW over the same horizon.

Meanwhile, the United States is aiming for only about 85 GW. Although there is less visibility on China’s road map, offshore wind could help accelerate the end of coal power — improving air quality and ensuring energy security along the way.

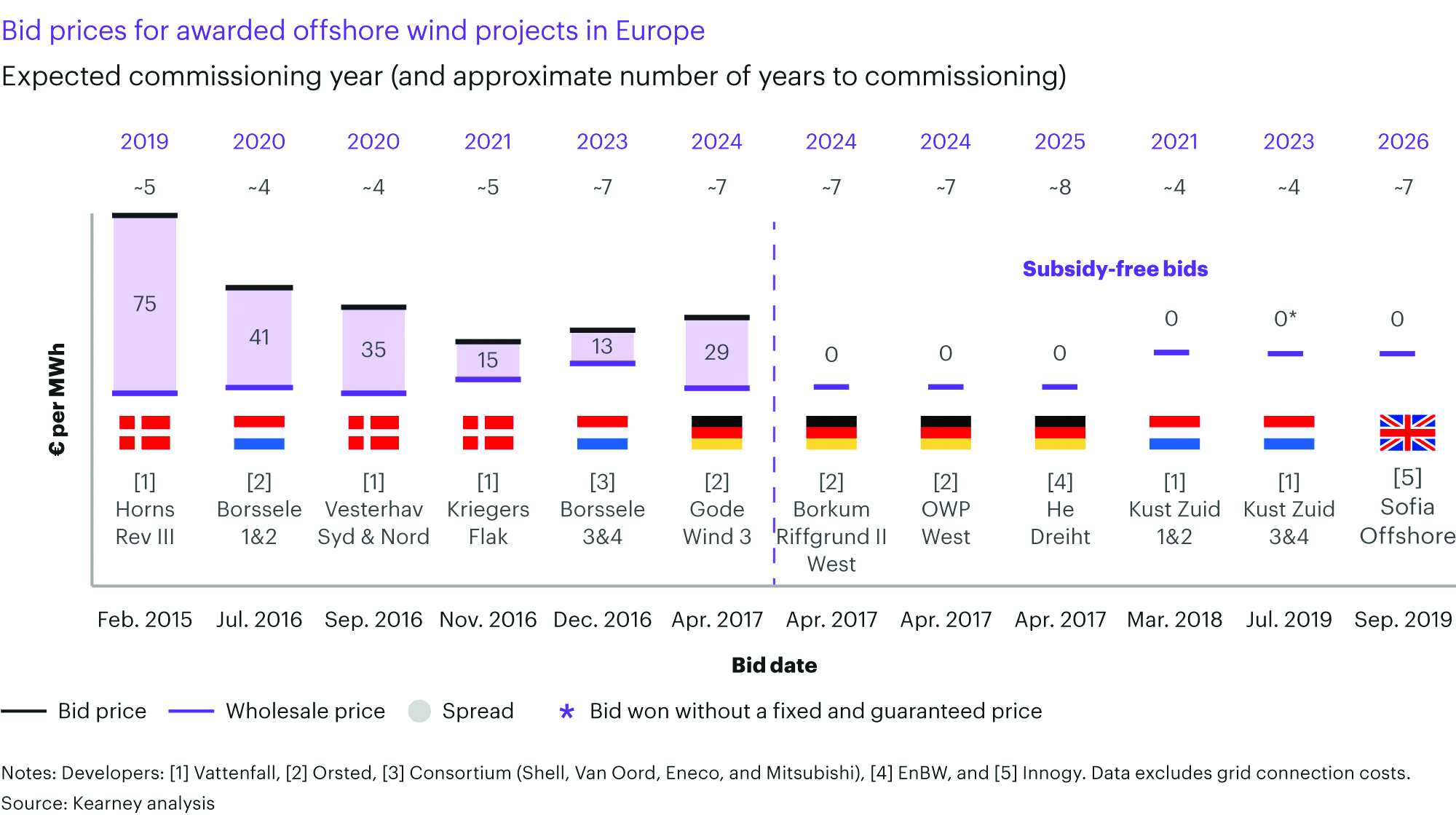

Figure 1: Subsidy-free bids illustrate the competitiveness of offshore wind projects.

Competitive economics

The economics of offshore wind are improving as the costs come down, and the energy source becomes more competitive with not only fossil fuels but also other renewable technologies, including solar photovoltaics (PV) and onshore wind. [2] As wind turbines grow (up to 12 MW and already announced 15 MW), the load factor could reach new records — greater than 60 percent — making offshore wind technology even more cost-competitive in the future. The International Energy Agency (IEA) predicts a sharp decline of offshore wind’s levelized cost of electricity (LCOE) until 2040, down from about 150 euros per MWh to 25 euros to 45 euros MWh depending on the geographic setting. [3] This has enabled a key change with the emergence of subsidy-free bids (see Figure 1). [4]

Huge energy potential

Despite significant growth over the past several years, mostly in Europe, offshore wind is still a very small share of world power production (68 GWh in 2018, or about 0.3 percent) and installed capacity (28 GW in 2018, or about 0.4 percent). [5] Technical sources offer a power potential of more than 25,000 GW globally, with the United States having the largest offshore wind technical potential both for near-shore and far-from-shore zones (more than 10,000 GW).

Offshore wind capacity is expected to grow by about 25 GW per year over the next two decades, activating a limited share of technical potential. [6] Furthermore, offshore wind is displaying strong resilience amid the COVID-19 pandemic with annual capex expected to equal offshore oil and gas capex both in Europe by 2021 and in the United States over the next decade. [7]

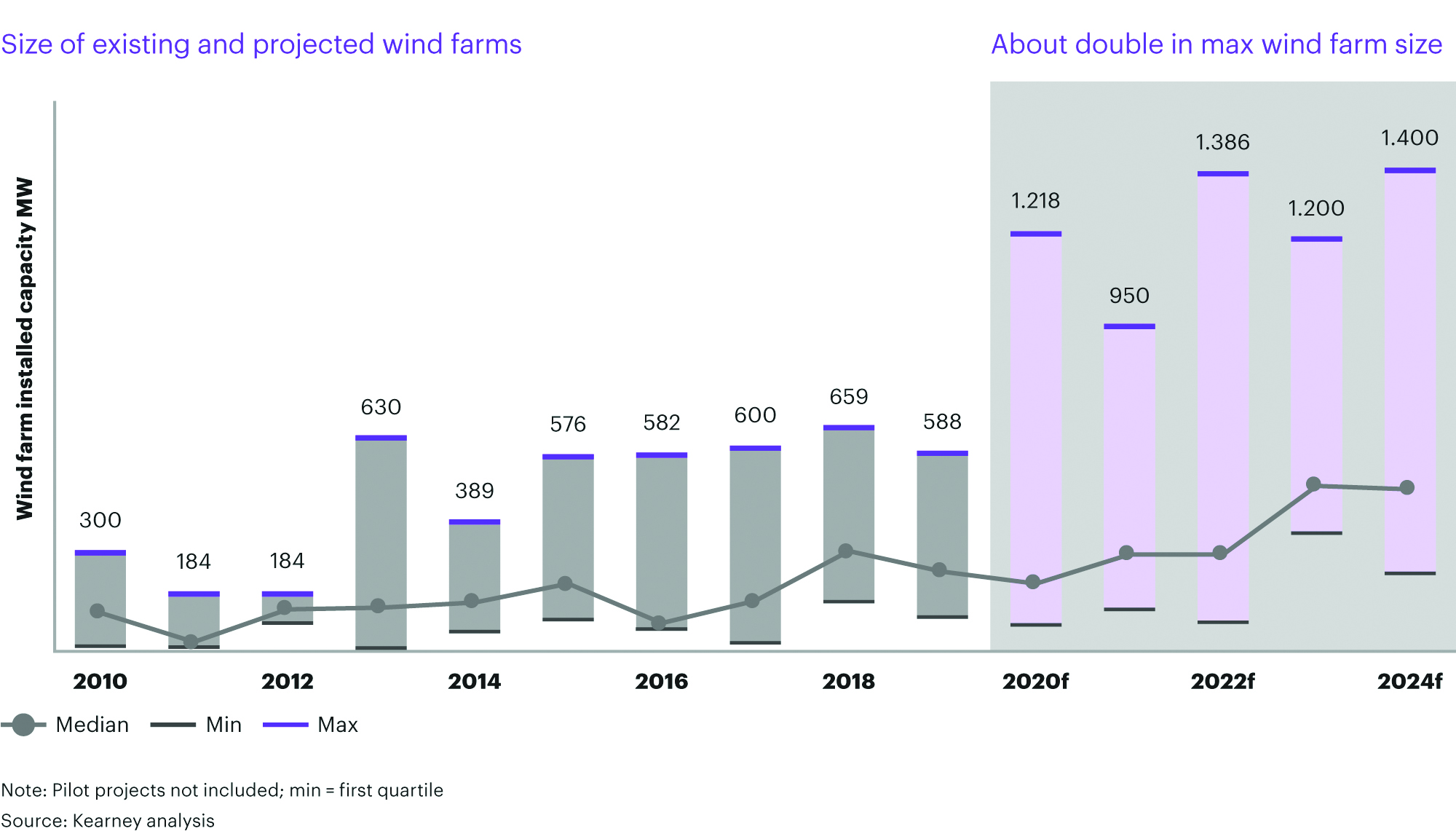

Figure 2: Offshore wind farms are getting much larger.

Market dynamics are creating new tensions in the offshore wind industry

Attractive growth prospects are creating complexities and challenges in several areas.

The development of offshore wind is influenced by local market factors, and countries are adopting a variety of approaches to foster renewables growth: [8]

Energy security: This is a key incentive for the EU, but the United States is less concerned despite benefiting from the world’s largest source of offshore wind. The EU has defined a clear ambition with a strong commitment from countries and structured supporting policies, including the Green Deal, potentially boosted by the Next Generation EU recovery plan.

Wind turbine manufacturing capacity: This is well-established in the EU, with leading capacities already deployed in the North Sea. In the United States, offshore wind is still an emerging market, with only 30 MW of installed capacity in the first half of 2020.

In the United States, despite strong fundamentals such as the technical potential and support mechanisms, full development of the offshore wind value chain is far from achieved and will require structured support. In China, offshore wind should benefit from a centralized administration, adequate infrastructures, potentially huge wind-turbine manufacturing capacities, and logistics capabilities. This implies short contracting procedures, government support, and no public acceptance issues.

Power grid flexibility and regulation: These areas could provide additional complexity and embed various integration capacities, such as grid connection technologies, bidding processes and contracts, merit order, and support mechanisms for connection costs. Even if some countries already have reached their integration capacity, the European network is very well integrated, providing additional capacity for offshore wind integration. The U.S. power grid is fragmented and has a limited capacity to deal with a large share of intermittent electricity. China’s power grid is integrated, which would favor the integration of wind power. Finally, large hydro-storage capacities provide the ideal combination with wind offshore.

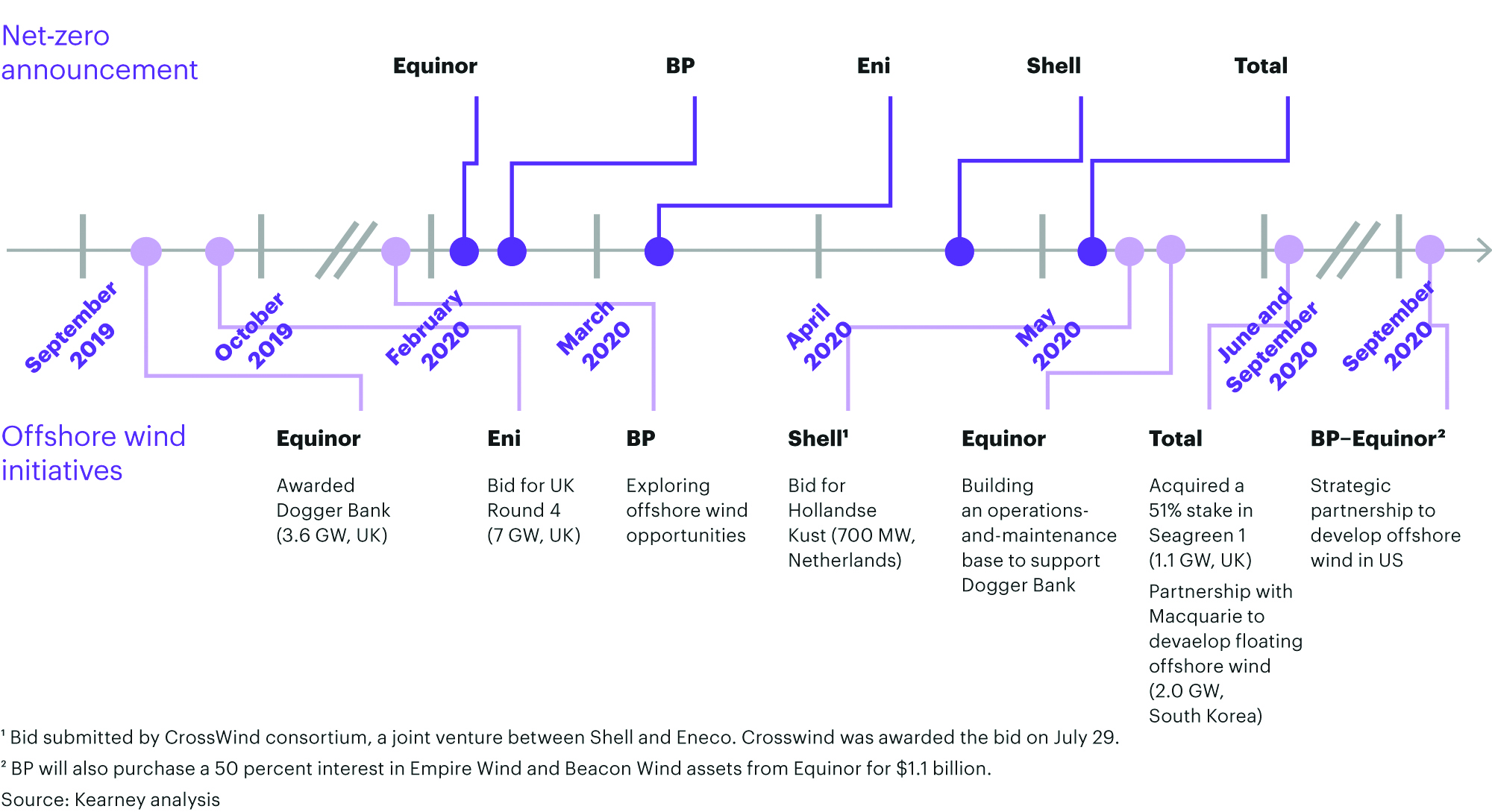

Figure 3: Aiming to achieve their net-zero targets, oil and gas companies are entering the offshore wind business.

Larger and more complex scope

This year marked a step change in the size of wind farms, with the largest wind-farm size doubled compared with past years (see Figure 2). In addition, hybridization with other technologies will be crucial for economic and environmental viability. Recent bids show a combination of offshore wind with green H2 (electrolysis). For example, in July of 2020, Shell and Eneco were awarded a tender to create a wind-farm-powered green hydrogen hub. [9]

On the technology side, floating solutions can unlock additional upsides. They address the largest technical potential of offshore wind (72 percent of offshore wind’s technical potential is in deep water) and higher load factors, driven by better wind conditions. In addition, floating solutions enjoy better acceptability and reduce usage conflicts with other sea activities, such as fishing, coastal navigation, and recreation. However, several challenges are yet to be addressed, including the high upfront cost and long project timeline, the infrastructure needed to assemble turbines, and full-scale testing and demonstration (coping with pitching and rolling, resisting harsher weather conditions, and handling cable complexity). The design of floating solutions is also still at an early stage of development.

Increasing competition and key players’ strategic moves

The offshore wind landscape is becoming more crowded with several new entrants along the value chain. While traditional players are pursuing aggressive growth to stay ahead of the game, solid new entrants are reshaping the offshore wind landscape. [10] The net-zero boom hit the oil and gas majors in 2020, with Equinor followed shortly by most peers. To support their net-zero targets, oil and gas operators are walking the talk with several offshore wind initiatives launched over the past year (see Figure 3).

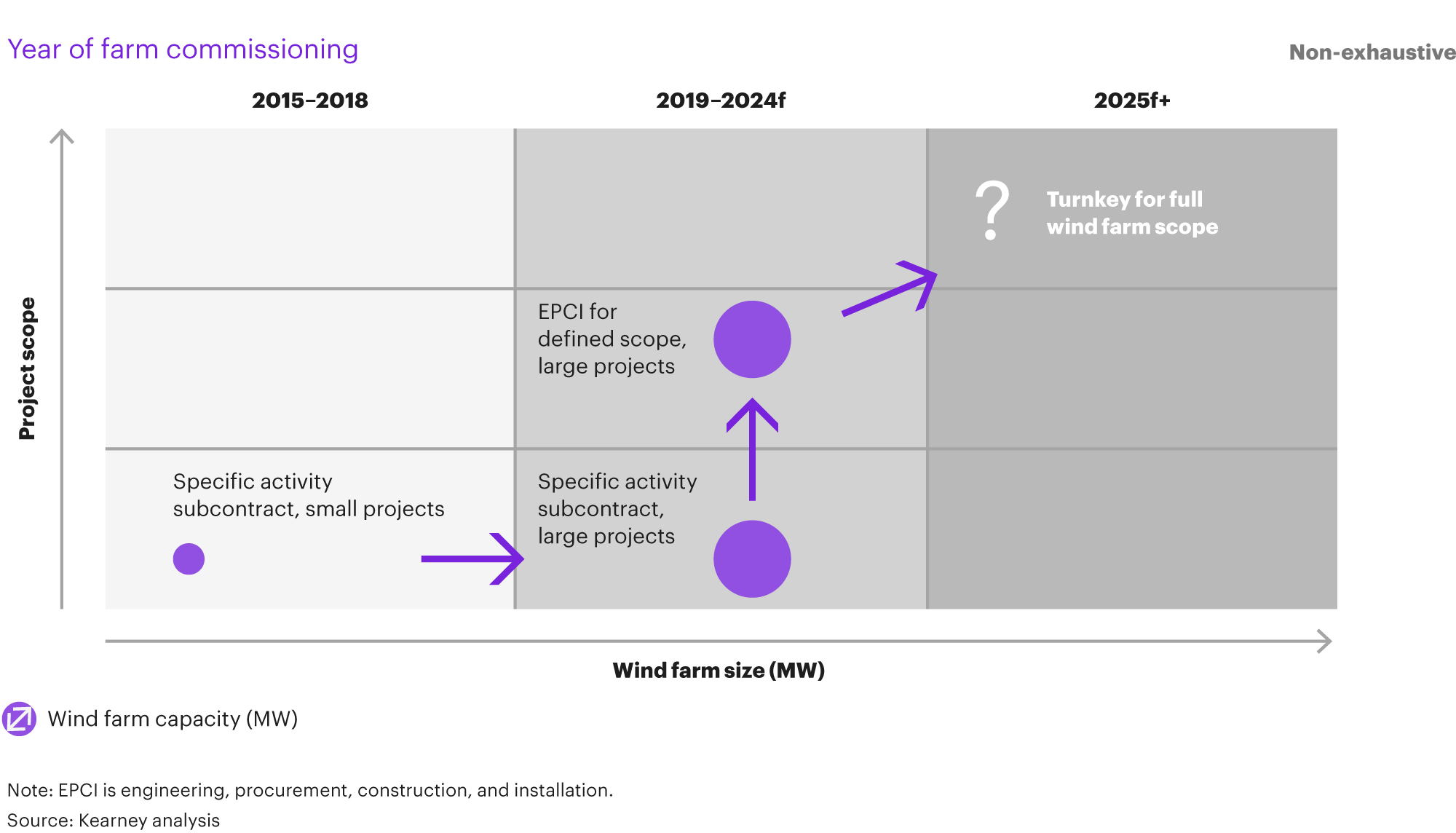

On the project development side, traditional oilfield services and engineering, procurement, and construction (EPC) players are capitalizing on their offshore capabilities and diversifying into offshore wind (see Figure 4). Traditionally, oil and gas EPC had been marginally involved in offshore wind projects as subcontractors for specific activities with limited scope, such as installing foundations for pilots or small wind farms. Now, they are repositioning in the value chain to deliver larger, more complex project scope — from subcontracting for large wind farms to taking on engineering, procurement, construction, and installation (EPCI) roles for a defined project scope. In the future, the role of EPC players may evolve to deliver turnkey projects for a full wind farm, with examples so far only seen in Asia.

Figure 4: Role of oil and gas EPC firms in offshore wind.

Potential supply chain bottlenecks

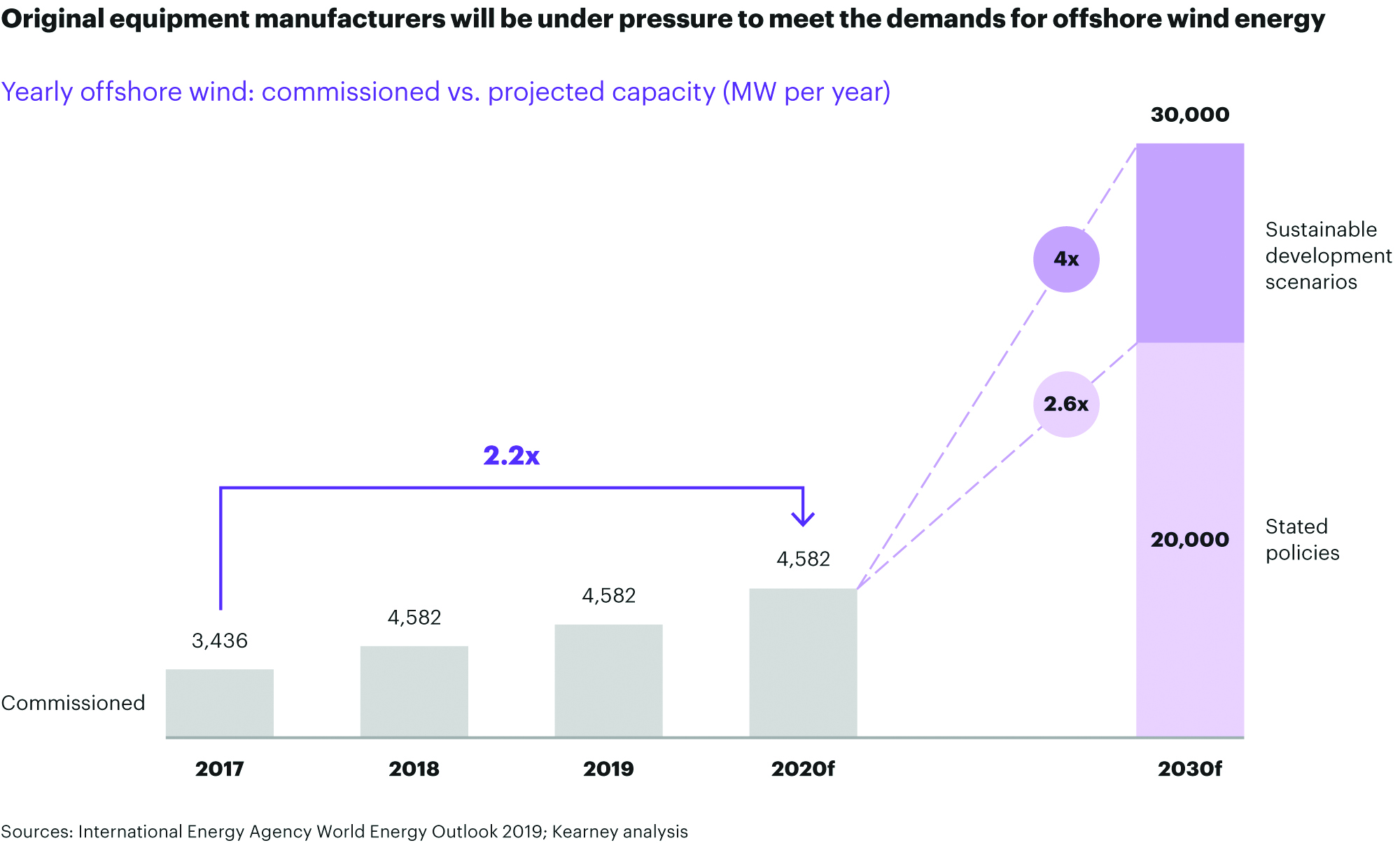

Delivering the potential will most likely stretch the value chain, with bottlenecks for turbine production and logistics. The first question will be about whether original equipment manufacturers (OEMs) have the capacity to expand production to meet demand. Over the past several years, OEMs delivered an annual installed capacity of about 7 MW, but demand will grow to about 20 to 30 MW per year until 2030 (see Figure 5). This gap could be even wider depending on OEMs’ financial situation. In parallel, high demand in marine logistics (offshore vessels) could create scarcity and tension on prices.

How to win the new gold rush

As discussed, offshore wind energy is a strong candidate for massive growth in some regions. However, an array of market dynamics is creating tensions that are affecting the value chain and creating potential bottlenecks that could affect the overall outcome of projects. Winning the new gold rush will require taking a systematic and collaborative approach.

Choose your battles

The first priority is to identify the sites that have the highest strategic value for your objectives, including growth targets, the portfolio, and the footprint. It will also have implications for local factors, such as grid connection technologies, bidding processes and contracts, merit order, support mechanism, and time to operations, as well as for regulations, such as the Urban Planning Code authorization for building turbines of more than 12 MW.

Bidders will need to master the contracting process across countries and regions, including understating the prerequisites and differentiating elements to win the bid. The competition is getting tougher. For example, in the Dunkirk wind-farm award, the top five bidders all scored very closely in the tender criteria, with a slightly bigger difference in the bid price: 44 euros per MWh for the winning and between 47.5 euros and 51 euros per MWh for the others. [11]

Figure 5: Original equipment manufacturers will be under pressure to meet the demands for offshore wind energy.

Streamline the wind-farm delivery model

Delivering much larger and more complex wind farms requires moving away from the traditional master-servants project development approach with its many siloed interfaces. Collaborative design optimization could significantly reduce costs and fast-track the time to market. Offshore could unlock significant value by taking advantage of lessons learned from other industries, such as automotive, aerospace and defense, and electronics. While the oil and gas industry has traditionally struggled to do so, offshore wind has the features needed to be successful, with strong standardization potential and flexibility for lean design (lacking heavy legacy specifications).

A new delivery approach also requires new business models and new ways of working. Strategic alliances are a win-win for operators, OEMs, and EPC to tackle the following elements:

Improve the project economics by working together to address large cost areas, taking on the full envelope of costs and seeking to bring it down as opposed to traditional sourcing requests for proposals (RFPs) that are focused on price and likely to increase with change orders.

Reduce cycle time by accelerating execution and avoiding RFP and tender processes.

Develop technological synergies with contractors by engaging them in advance to elaborate on designing an optimal solution.

In a capacity-constrained environment, strategic alliances also offer opportunities to secure material and services while giving suppliers certainty about revenues. Oil and gas players (operators and EPC) can also capitalize on their strong offshore experience. Repurposing assets and reskilling the workforce require a new cross-business portfolio view and management, such as multipurpose vessels serving oil and gas platforms and wind farms, and talent management, such as sharing resources across oil and gas and wind projects.

Achieve operational excellence

Operators will need to assess and extract the wind farm’s true potential. With more pressure to reduce costs and with subsidy-free bids becoming the new norm, operational excellence is paramount to maximizing profitability. Smart operations are a must to optimize both the top and bottom line by considering a broad set of parameters, such as revenues, cost of spare parts, market dynamics, regulations, turbine downtime, weather forecast, and operations and maintenance costs. Advanced analytics could allow for precisely predicting the impact on costs and revenues to inform decision-making and optimize profitability.

Predictive maintenance enables striking the right balance between corrective and preventive costs, including the costs of failure, reducing total expenditures, and increasing availability and reliability.

Digital twins can extend the life of assets by combining operational and physical inputs, such as inspection information and mechanical characteristics, with advanced simulation, such as fatigue analysis, inspection plan, and predictive maintenance. In addition, using digital twins in the engineering phase could optimize design and reduce material and installation costs.

Squeeze financial value

Finally, operators will need an integrated approach to optimize their financial value.

Value pools: The boundaries between sourcing, trading, and production are blurring, driven by demand response, batteries, and decentralized generation. New value pools are emerging from all parts of the chain. Contractual and physical flexibility to match supply and demand and balance the grid, such as capacity contracts, virtual storage, and options and derivatives, drives portfolio optimization and provides growth opportunities. The operating model needs to adapt to allow an integrated steering of power assets, such as renewable, storage, and combined cycle gas turbines, and consumption, such as internal and external, by location, minimum and maximum load, and steerable load.

Decision-making: With renewable energy growth, the power market is becoming more weather-driven, and demand for flexibility is moving toward the short term. Consequently, the speed and quality of decisions are paramount to ensure smooth alignment between power assets and consumers, such as scheduling and re-dispatching processes with assets and consumers to avoid imbalance costs and capture market opportunities as well as increased frequency balance to manage renewables generation unpredictability. To support quality and efficient decision-making, information system infrastructure and data management are crucial to achieve the following:

Combine massive amounts of data in real time.

Develop robust data analytics for optimization (analytical models with accurate signals, confidence estimation, and visualization).

Define the trade-offs for result accuracy versus computation speed.

Ensure seamless interactions between independent information systems and functionalities.

Define the trade-offs between multiple performance models vs. a full integrated model, such as individual turbines, wind farms, and country-level portfolios.

Facilitate internal and external data exchanges.

Think big and act fast

The economies of scale for large wind farms (more than 1 GW) is the new norm for cost-competitiveness. All players are moving. To leapfrog the competition and not get left behind, it is imperative to quickly screen and target opportunities. Where to start will depend on players’ maturity. In any case, it is important to accelerate the learning curve. For new entrants, this may mean starting with smaller roles or a smaller scope and quickly transitioning to larger, more complex ones.

Choose your partners, and nurture the collaboration

Winners will play a team game with strategic alliances and collaboration across the value chain. This will ensure delivery capacity, such as turbine production, installation, and footprint as well as best-of-breed skills, such as technology and knowledge, while accelerating innovation. A cultural fit and collaboration framework will be essential to success.

References

European Commission Climate Action Tracker.